New Analysis Looks at How OBBBA Will Impact Government Costs of Federal Student Loans

By Maria Carrasco, NASFAA Staff Reporter

A new analysis examines how the implementation of the One Big Beautiful Bill Act (OBBBA) will reduce the government's costs for federal student loan programs, in part due to the new Repayment Assistance Plan (RAP) and the elimination of the Graduate PLUS loan program.

The analysis, conducted by the Committee for a Responsible Federal Budget (CRFB), examines a recent Congressional Budget Office (CBO) report on the costs of federal credit programs in 2026.

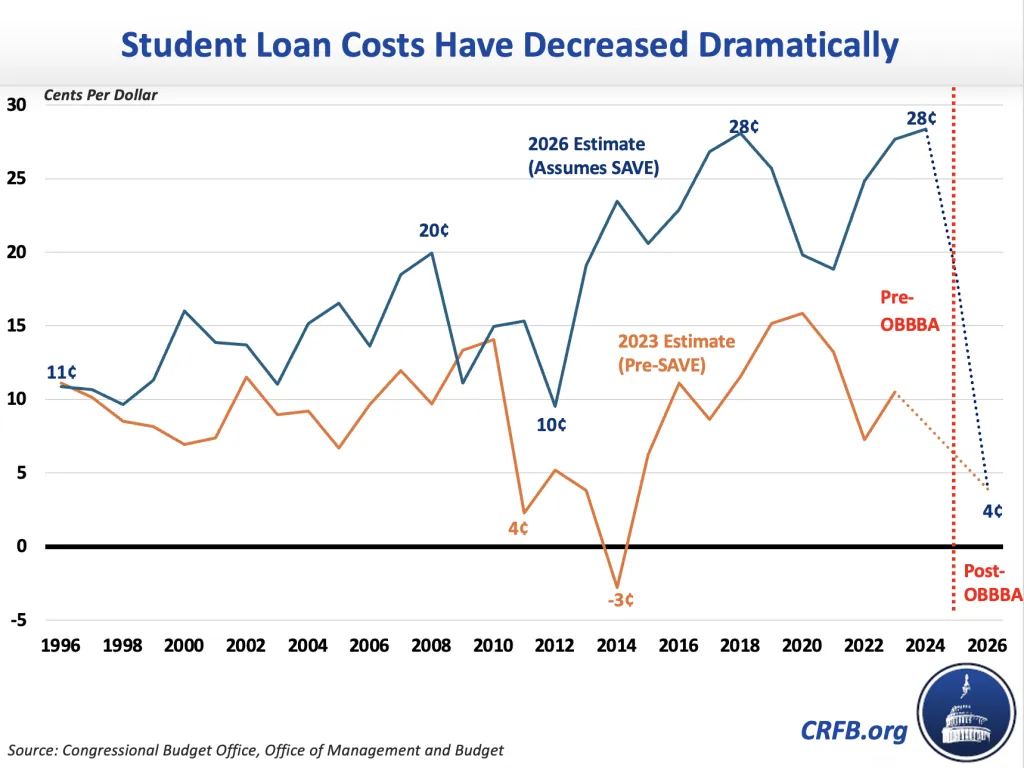

In its analysis, the CRFB notes that the federal government will lose 4 cents per dollar lent in 2026, on a present-value basis. This is compared to 2025, when the federal government lost 18 cents per dollar lent.

The CBO also projects that the subsidy rate for new student loans will drop to 4%, which would be one of the lowest rates for a cohort of loans since the creation of the Direct Loan program, CRFB notes.

A big part of this cost reduction is the implementation of the new RAP, an income-based repayment plan that becomes effective on July 1, 2026, and is part of the OBBBA. With the creation of RAP, current borrowers will be moved out of some of the other income-driven repayment (IDR) plans – Saving on a Valuable Education (SAVE), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR) – by 2028, after which they will be sunsetted.

The report also compares projected cost savings for undergraduate loans across repayment plans, estimating that current income-driven repayment (IDR) plans cost about 37 cents per dollar lent, whereas under the proposed RAP structure, the cost drops to roughly 10 cents per dollar.

Notably, this comparison relies in part on projected subsidy rates for the SAVE plan. However, it’s worth noting that key SAVE provisions, including the expanded income exemption (225% of the federal poverty guideline, up from 150%), reduced payment amounts, and the full unpaid interest subsidy, were never fully implemented due to ongoing legal challenges. As a result, the fiscal impact of SAVE as modeled in this report differs from what borrowers actually experienced. Comparing the projected cost/savings of RAP to a version of SAVE that was not fully operational may overstate the magnitude of savings. Additionally, including subsidy rates from the temporary pandemic-era repayment pause further complicates the comparison, as those rates reflected extraordinary, time-limited policies rather than a stable, long-term repayment framework.

The CBO, in its report, estimates that borrowers will pay more under RAP than they would have under the IDR plans eliminated by the 2025 reconciliation act (OBBBA), and that, as a result, the costs of student loan programs as a whole will be lower.

Beyond the creation of RAP, another reason for this estimated reduction in costs is due to the elimination of the Graduate PLUS loan program and new loan limits on graduate programs under OBBBA. Though it's unclear how much new graduate loans will cost the government, CRFB notes that the government loses 27 cents per dollar lent under the Grad PLUS program.

However, as an alternative projection, CRFB notes that under fair-value accounting, which incorporates market risk into the calculation and better matches the benefit relative to a private loan, the student loan program could cost the government 18 cents per dollar lent.

The CRFB is a nonprofit, nonpartisan organization that advocates for public policy to reduce the federal budget deficit and lower government spending. In the report, the CRFB applauded the OBBBA’s effort to lower government spending.

Publication Date: 2/18/2026

Ben R | 2/19/2026 8:32:51 AM

This is a projection of costs based only on newly issued loans this year and the new RAP plan. It does not account for costs of previously issued loans, which are much higher due to a variety of factors. It also does not consider the heavy use of forbearance on aging loans or $0 payments under legacy IDR plans. Loans over 10 years old with no payment history due to extended periods of non payment are considered as fully collectable as brand new loans.

Stephen B | 2/18/2026 9:37:05 AM

At page 11

For borrowers enrolled in fixed-payment repayment

plans, subsidy rates in 2026 are projected to vary from

−24.8 percent for the PLUS loan program for graduate

students to 11.8 percent for the subsidized Stafford loan

program—both calculated on a FCRA basis.

The question becomes what percentage pay under the various IBR Programs and RAP?

WIth fixed payments, the federal government makes money, with RAP they lose

You must be logged in to comment on this page.